Retailer Commitments, 2026 and the Implications for a 2032 Cage Ban

Published on : 27 Feb 2026

The report was capturing retailer thinking as it stood at that point and assessing the possible implications for production systems.

When BFREPA commissioned ADAS in 2017 to assess the likely impact of retailer commitments to move away from cage eggs, the study was rooted in a very specific moment in time. The predictions were based on stated sourcing intentions gathered through individual meetings held during 2017. As the executive summary of the report makes clear, “the overall aim of this study is to provide clarity on the current thinking of these retailers and to assess the likely implications of changing purchase policies.”The projections within the report therefore flowed directly from those retailer discussions rather than from an independent market forecast of structural change.In other words, the report was not forecasting a legislative outcome. It was capturing retailer thinking as it stood at that point and assessing the possible implications for production systems.It is important to remember that non cage commitments had only recently been made at that stage. Retailer policies were still evolving. Page 16 of the 2017 report notes that while some retailers were already engaging with suppliers on implementation plans, for others “it is clear that intentions and plans are still at a very early stage and that detailed discussions with suppliers are yet to take place.” The “current thinking” referred to in the executive summary was therefore emerging rather than settled.This context is important, because it illustrates that the assumptions around future system growth were being formed during a period of transition rather than at a point of settled commercial certainty.The 2020 update to the report did not include refreshed discussions with retailers to establish whether their thinking had shifted materially since 2017. As a result, the later document continued to reflect assumptions rooted in those earlier conversations.In relation to barn production specifically, the executive summary of the 2017 report acknowledges uncertainty at the outset. It states: “At this stage, certain key issues are unclear. These include the extent to which there will be significant growth in barn egg production and thus the likely impact on the free range egg production sector.” The assessments reflected views expressed in retailer meetings and the general industry understanding at the time. Key uncertainties identified in relation to the future role of barn included production systems, system longevity, consumer awareness and reaction, and pricing.Those acknowledged uncertainties help explain why the anticipated large scale expansion of barn production did not ultimately materialise in the way some scenarios suggested.The calculations in the 2017 report were therefore based on retailer views and industry data available at that time, and the uncertainties were explicitly recognised. They were assessments of likely implications under a developing set of retailer commitments, not projections of a fixed or finalised policy environment.

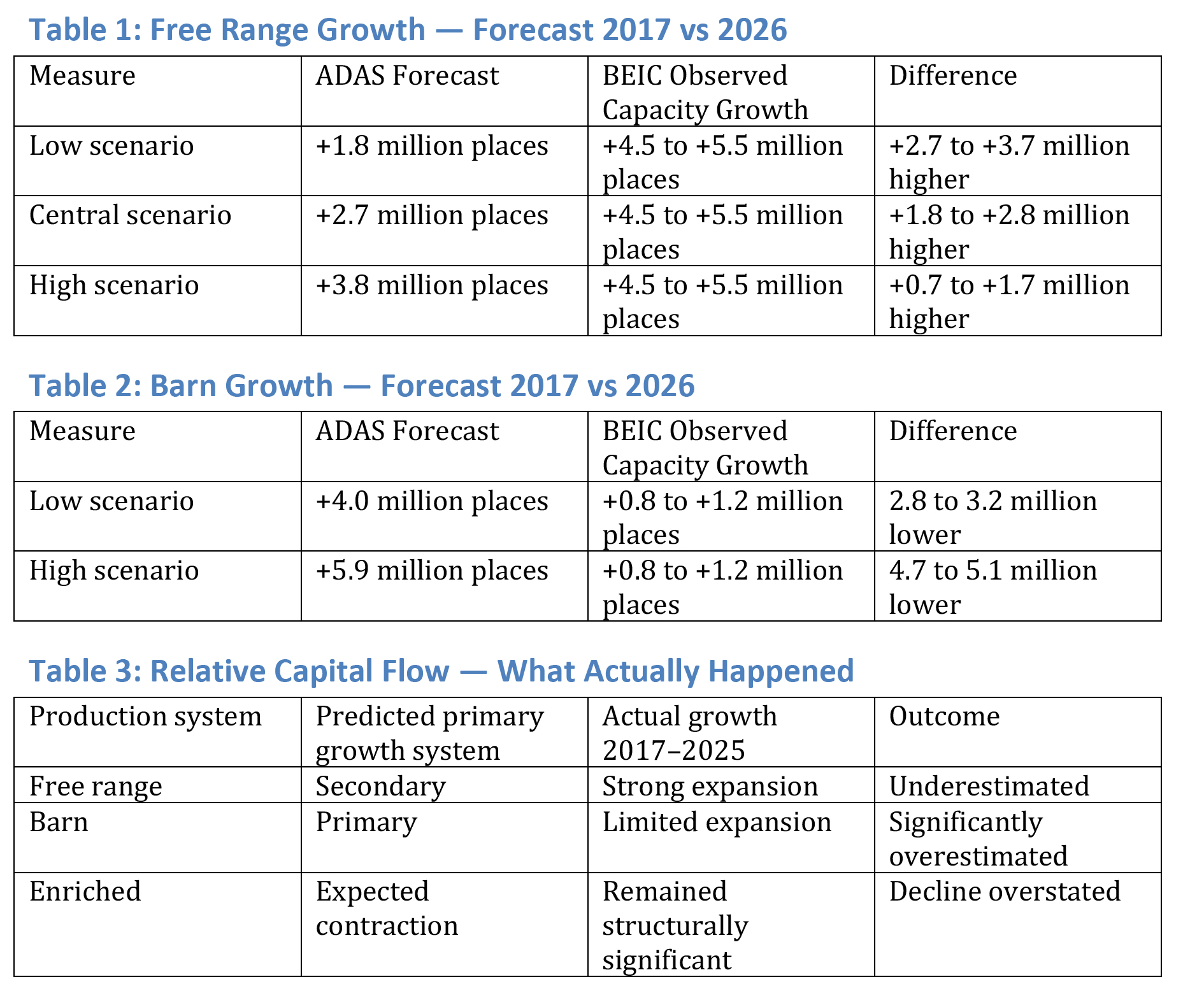

These tables demonstrate clearly that capital flowed disproportionately into free range rather than barn.

Against that backdrop, and with BEIC production system data now available through to the end of 2025, it is possible to examine how those early assessments compare with what actually happened.The ADAS work assumed that approximately 4.3 million cases of enriched cage eggs would be displaced from the retail market by the end of 2024. The central analytical question was how that volume would be replaced domestically. Barn was identified as the principal successor system for value eggs, with a projected requirement of between 4.0 and 5.9 million additional barn places. Free range was expected to grow more modestly, with forecasts suggesting a need for between 1.8 and 3.8 million additional free range places.With BEIC capacity data now available through to the end of 2025, we can compare those forecasts with actual system growth between 2017 and 2025. The comparison focuses on incremental growth, mirroring the way the original forecasts were expressed.Free range capacity increased from just under 30 million birds in 2017 to approximately 34 to 35 million birds by 2025, an expansion of around 4.5 to 5.5 million places. Barn capacity, by contrast, increased only modestly, from around 2.5 to 2.8 million birds in 2017 to approximately 3.5 to 4.0 million birds by 2025 — growth of roughly 0.8 to 1.2 million places.The contrast between forecast and 2026 is stark.These tables demonstrate clearly that capital flowed disproportionately into free range rather than barn. This was not accidental. It reflected a number of factors including retailer behaviour, contract structures, a lack of visibility or consumer understanding of barn, producer confidence and potentially access to capital at the time i.e an investment in barn is appreciably higher than free range.At the same time, producers adapted in ways not anticipated by the assessments. Speciality eggs expanded, offering higher value alternatives rather than chasing volume. White egg production increased as producers sought feed efficiency and cost control within existing systems.Between 2017 and 2024, total UK egg consumption rose from 12.7 billion eggs to 13.6 billion, while per capita consumption increased from 192 to 199 eggs per person. This growth demonstrates that system expansion was occurring against a backdrop of rising demand rather than a static market. The industry was not merely reallocating supply between housing systems, but meeting a materially larger overall market.The growth in white egg production was not solely a producer led preference but reflected retailer specification, manufacturing demand and the efficiency advantages associated with feed conversion and persistency of lay. In particular, longer lay cycles in white flocks increased total egg output per bird housed, supporting supply growth without a proportional increase in hen numbers.The original work focused on housing systems rather than breed economics, yet biological adaptation became an important part of the industry’s response.Crucially, enriched production did not disappear. Retailer commitments removed cage eggs from many supermarket shelves, but they did not eliminate enriched production across the wider market. Displaced retail volume was diverted into foodservice, wholesale, manufacturing, export markets and retail channels not party to the commitments. This was a reallocation of routes to market, not a prohibition.The divergence between forecast and reality also cannot be understood without considering the wider structural shifts that occurred after 2017.Welfare frameworks evolved. Changes within RSPCA Assured standards, including developments around free range management expectations and retailer interpretation of assurance positioning, influenced system choice and cost structures. In some cases, evolving welfare requirements strengthened the strategic case for free range over barn.The period after 2017 was marked by unprecedented external shocks. The Covid pandemic reshaped foodservice and retail demand overnight. Eggs proved resilient, strengthening their position as a staple protein. This was followed by sustained food inflation. Rising feed, energy, labour and finance costs altered production economics. Yet rather than suppressing egg demand, rising prices across meat and other proteins reinforced eggs’ role as a relatively affordable source of nutrition.Avian influenza became a structural constraint rather than an episodic risk. Repeated outbreaks influenced placement decisions, housing requirements and capital confidence. The assumption of smooth, linear system substitution did not account for prolonged disruption of this nature.All of this context matters when considering the Government’s current proposal for a legislative cage ban from 2032. Unlike retailer commitments, a statutory ban removes enriched production entirely. It does not allow diversion into alternative channels. It compresses timelines and removes commercial flexibility.Alongside the consultation, Defra has published what it terms a De Minimis Assessment, meaning the department currently estimates the overall annual cost to business falls below the threshold that would normally trigger a full Regulatory Impact Assessment. That classification does not suggest there will be no impact on individual producers, but reflects the department’s current national level cost estimate. The BFREPA ADAS costing report is referenced in the document on page 21.Industry representatives have expressed concern that the conversion and capital build costs required to transition from enriched systems may be materially higher than those currently reflected in the national cost estimate. Questions have also been raised regarding the treatment of substitution effects, wider supply chain impacts and the valuation of consumer willingness to pay within the economic assessment framework.To understand the scale of that intervention, the arithmetic must be set out plainly. Enriched colony capacity currently stands at around eight to nine million birds, although the number housed now stands at 5.5 million. With an average free range shed accommodating approximately 32,000 hens, replacing that capacity domestically would require roughly 260 to 280 new free range sheds.This replacement calculation assumes that national egg consumption remains constant. However, given the increase of nearly 900 million eggs annually since 2017, any continued growth in demand during the transition period would require additional capacity beyond simple system substitution. The infrastructure challenge may therefore be materially greater than a straightforward replacement model suggests.Spread over five years, that equates to more than fifty new sheds per year, on top of normal replacement building and against a backdrop of planning constraints, environmental restrictions, grid delays, labour shortages and capital pressure.In addition to cost concerns, industry voices have highlighted the practical challenges associated with planning consent timelines, capital finance availability and regional development constraints. In some areas, planning determinations can extend for many months or longer, creating uncertainty over whether replacement capacity could be delivered within the proposed transition period.By comparison, the five million free range places added between 2017 and 2025 were delivered over nearly a decade under market led conditions. Expecting a larger structural shift in a shorter timeframe, through legislative compulsion alone, would require fundamental reform of the planning system. Appropriate agricultural development would need to be fast tracked. Delays would need to be reduced. Consistency across local authorities would need to improve.There is a further distortion. The Government has extended tariff free access for Ukrainian agricultural products, including eggs and egg products, into the UK market. While the geopolitical context is understood, the market implications cannot be ignored.UK self sufficiency has improved but remains below full domestic coverage, and net imports continue to form part of total supply. In that context, tightening domestic production standards without equivalent alignment in trade policy risks increasing reliance on imported egg and egg products produced under different regulatory and welfare frameworks.Ukrainian egg production operates under welfare and regulatory standards that differ from those required of UK producers. Allowing tariff free imports from lower welfare systems while imposing additional structural costs on domestic production risks undercutting British farmers and exporting welfare responsibility rather than raising standards globally.If policy is to proceed, it must do so with clarity about infrastructure requirements, planning reform, trade coherence and realistic timelines. The industry has demonstrated its capacity to adapt. What it cannot adapt to is a mismatch between policy ambition and delivery reality.Any proposal to remove cages from UK production must also be matched by a genuine commitment to improving welfare standards across the whole market, not just within domestic supply. Welfare reform cannot stop at the border. If import policy cannot be adjusted to ensure that eggs and egg products entering the UK meet equivalent welfare standards, then the timetable for a domestic cage ban should be reconsidered until those policies align. Otherwise, the effect is not to raise welfare globally, but to displace production and transfer welfare responsibility beyond UK oversight.The experience of the past eight years shows that structural change in egg production is achievable when supported by confidence, coherence and realistic delivery frameworks. If the Government wishes to pursue a cage free future, domestic infrastructure policy, planning reform, trade alignment and welfare ambition must move in step. Without that coherence, policy risks weakening the very standards it seeks to strengthen.Producer Explanation – What Does “De Minimis Assessment” Actually Mean?Defra has published what is called a De Minimis Assessment alongside the laying hen cage reform consultation.In simple terms, “de minimis” means that, based on Defra’s initial estimates, the total annual cost of the proposal to business is below the government’s threshold that would normally trigger a full Regulatory Impact Assessment.That threshold is generally around £10 million per year in net costs to business.So at this stage Defra is effectively saying:They estimate the overall cost of the proposal to industry falls below that trigger level.Because of that, they have not produced a full formal Impact Assessment.The document has not been reviewed by the Regulatory Policy Committee, which would usually happen for larger regulatory changes.It is important to stress what this does not mean. It does not mean there will be little or no impact on individual producers.A policy can be classed as de minimis at a national level while still having very significant consequences for specific sectors or individual businesses, particularly those currently operating enriched colony systems.It is also worth noting that the BFREPA commissioned ADAS report on the retailers intentions is referenced in the document on page 21, which shows that our costings work is feeding into Defra’s thinking. However, whether the assumptions fully reflect current build costs, conversion costs, asset write-downs, and broader market realities is something producers are entitled to question.This is why consultation responses matter. If the real world costs of transition are higher than Defra has assumed, that evidence needs to be clearly set out.In short:De minimis does not mean “no impact”.It means government currently believes the overall cost falls below its formal assessment threshold.Whether that estimate reflects reality is precisely what the consultation process is there to test.CLICK HERE to download "The impact of buyers' intentions to purchase only non-cage eggs from 2025"CLICK HERE to download the "Update of the impact of retailers' non-cage commitments for eggs"CLICK HERE to download the "Consultation De Minimis Assessment"