Global feed grains outlook 2026: Stability masks rising volatility in global markets

Published on : 20 Apr 2026

Rabobank’s Nan-Dirk Mulder

Speaking to a large international audience at the World Egg Organisation conference in Warsaw, Rabobank’s Nan-Dirk Mulder set out a cautiously balanced but increasingly fragile outlook for global feed grains, with markets supported by strong supply but facing mounting pressure from geopolitics, energy and structural shifts in demand.At first glance, the market remains well supplied. Global stocks of corn and wheat are sitting at historically high levels across major exporting regions, while soybean availability has also been supported by record South American production, particularly in Brazil.That supply cushion is playing a key role in holding feed prices in check, even as external pressures build. Since the escalation of the Iran conflict, the global feed price index has edged higher, but the increase has been relatively modest compared with previous geopolitical shocks.

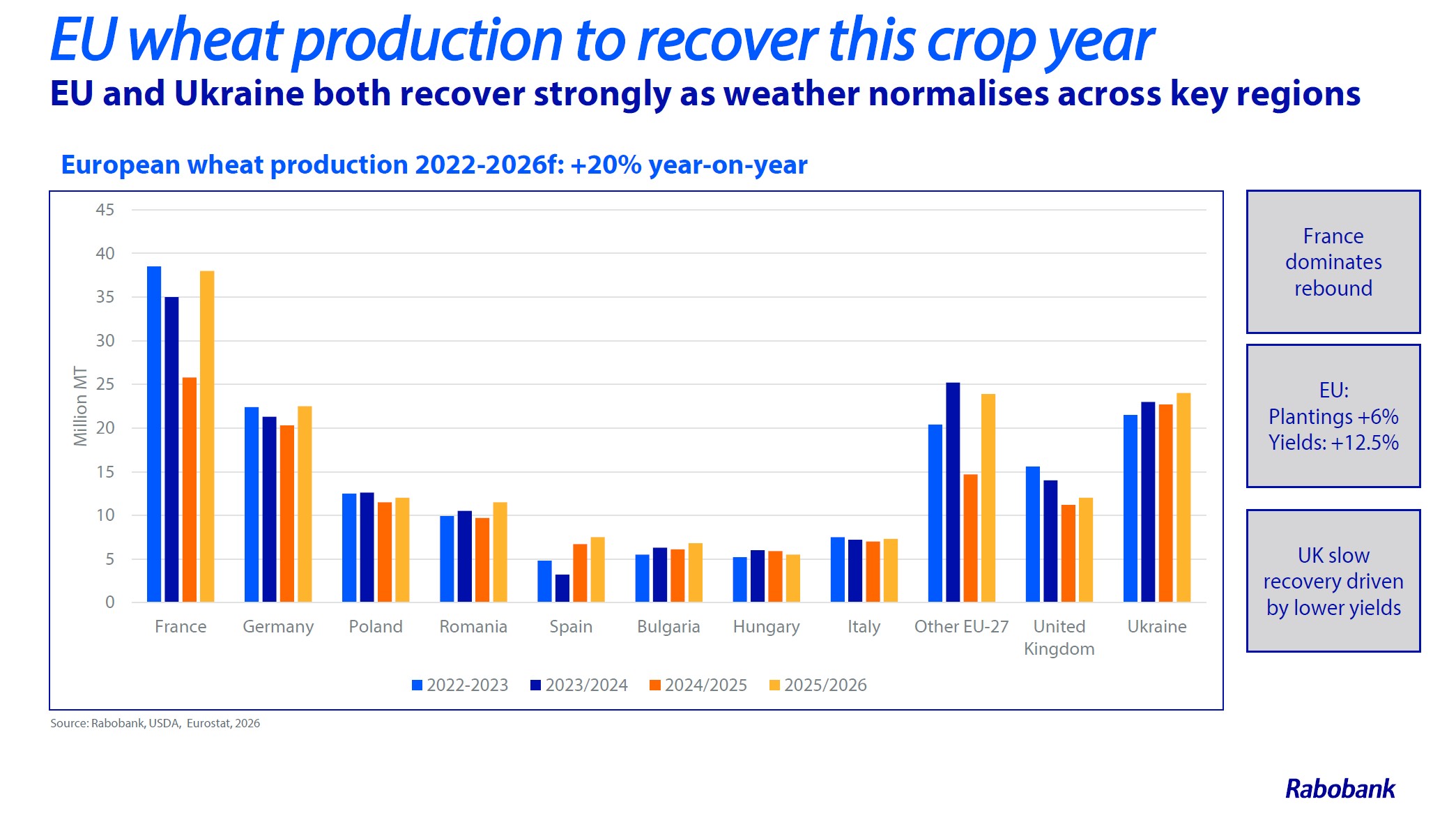

EU wheat production to recover this crop year

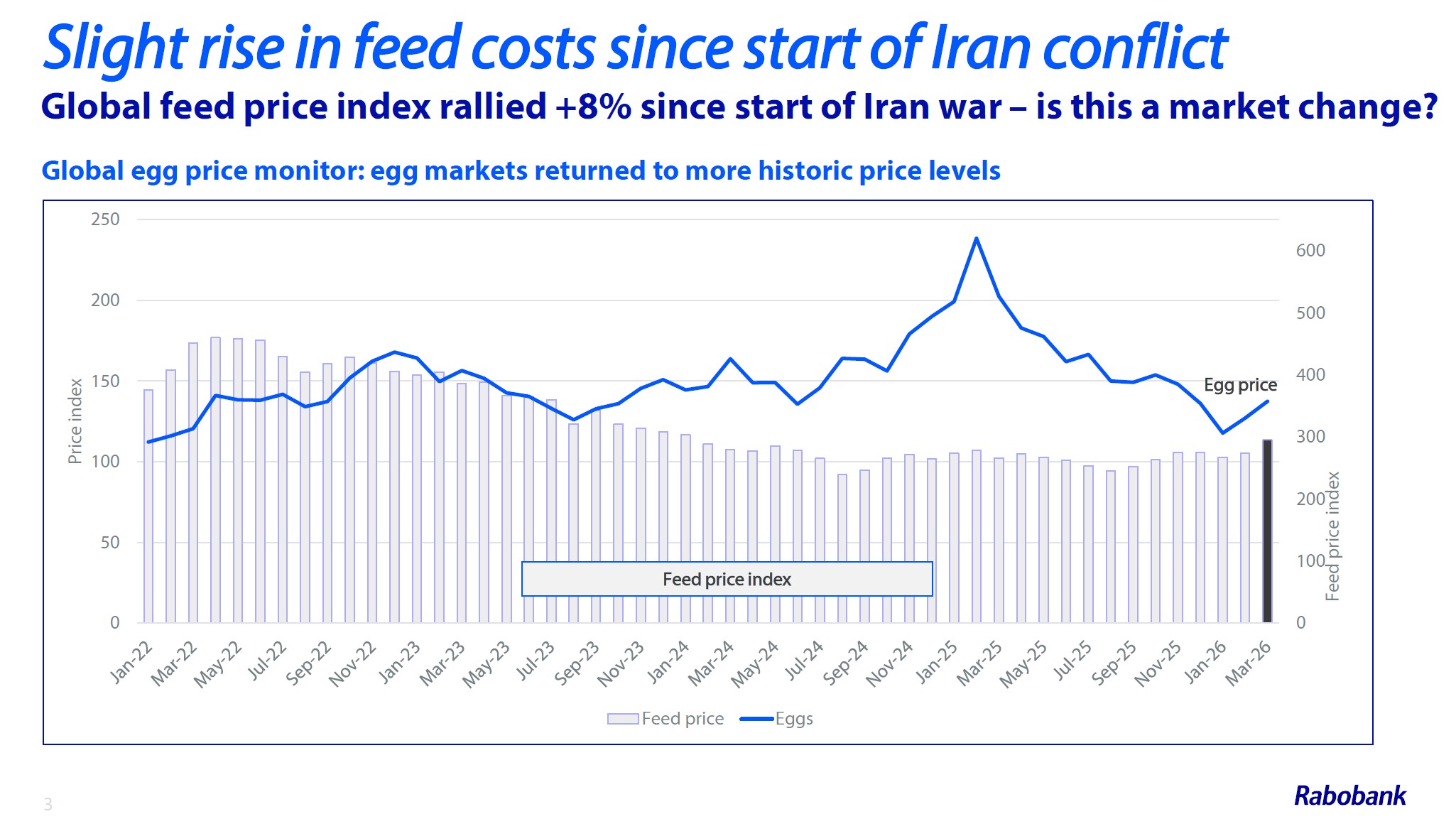

The early movement in feed costs reflects the initial impact of higher energy, fertiliser and freight markets rather than a full repricing of grain fundamentals. The presentation showed feed prices ticking upward while egg markets have largely returned to more typical levels, underlining that supply and demand remain broadly balanced for now.There are also clear signs of a lag in the system. Much of the increase in oil and input costs has yet to fully filter through into finished feed prices or livestock production costs, with forward purchasing, existing contracts and strong grain availability absorbing the immediate impact.

Slight rise in feed costs since the start of the Iran war

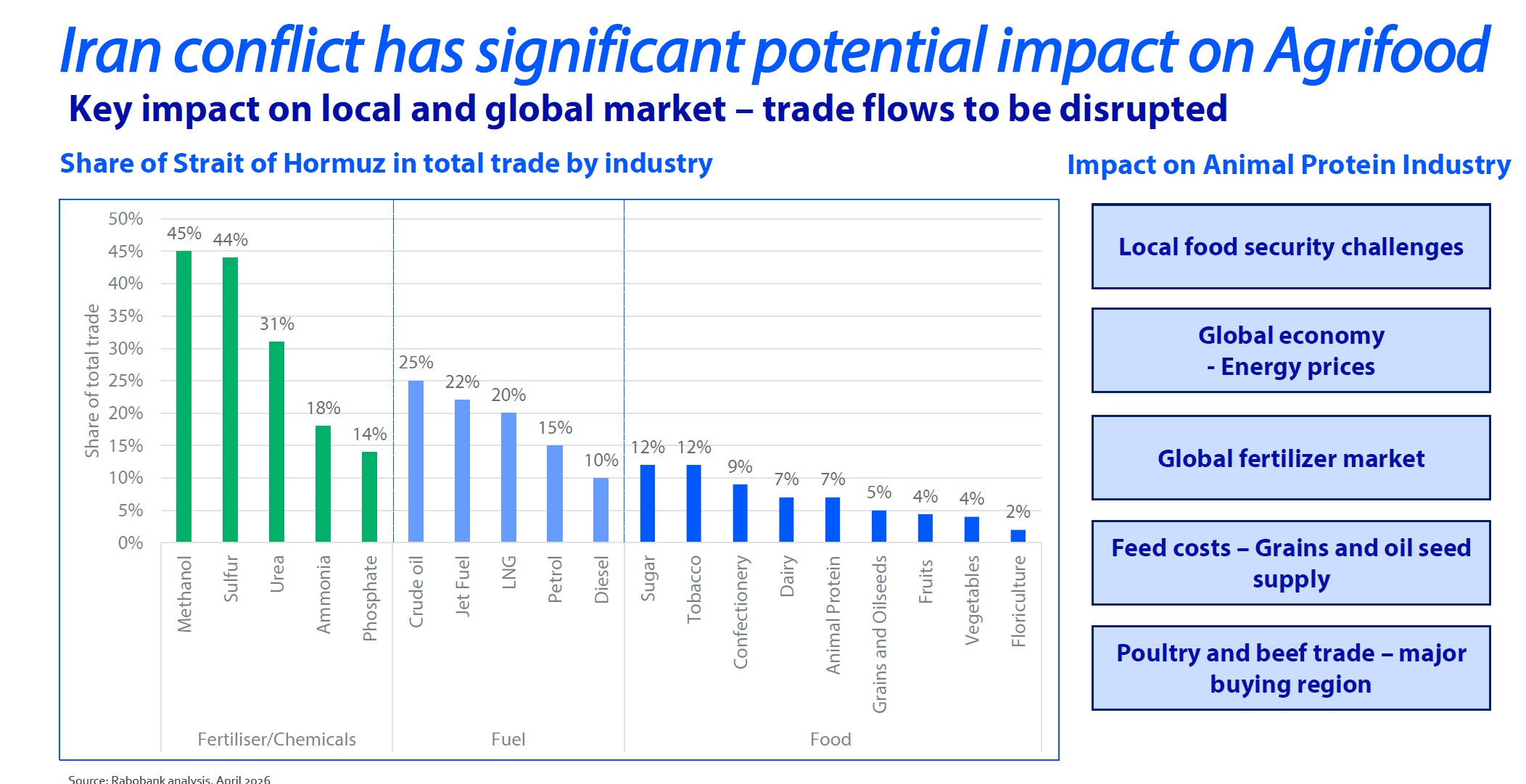

This creates a degree of short-term stability, but also leaves the market exposed. If disruption persists, particularly around energy flows and fertiliser supply, those higher costs are likely to become more visible later in the year as new crop decisions, input buying and feed formulation begin to reflect the changed cost base.Energy markets are once again shaping the direction of agricultural commodities. The link between oil and feed grains remains strong, driven through fertiliser production, fuel costs and biofuel demand. As oil prices move higher, those cost pressures feed directly into grain markets.The Strait of Hormuz has become a central risk point. Around 20% of global crude oil flows through the corridor, alongside significant volumes of fertilisers and agri-inputs.

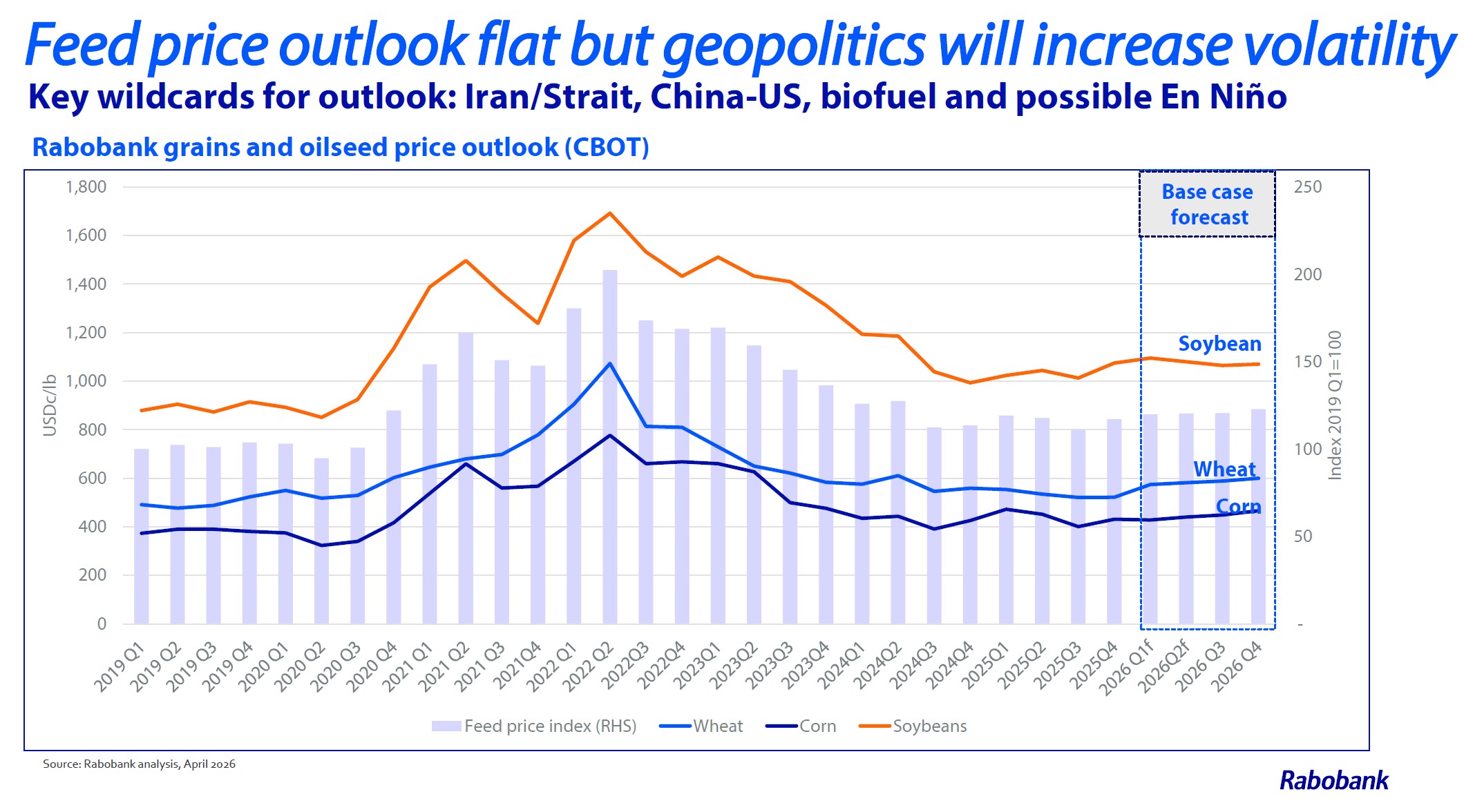

Feed price outlook flat

Short-term disruption has already affected shipping and air freight, while a prolonged closure would have wider consequences for input availability and crop production.Fertiliser markets are beginning to respond. Nitrogen prices have risen sharply in recent weeks, with urea increasing by more than 25% since the start of the conflict.That shift has direct implications for crop economics. Corn, as the most fertiliser-intensive feed grain, is particularly exposed, raising the likelihood of changes in planting decisions if high input costs persist. Soybeans, by contrast, require significantly lower nitrogen inputs, creating a clear incentive to adjust crop rotations if pressure continues.

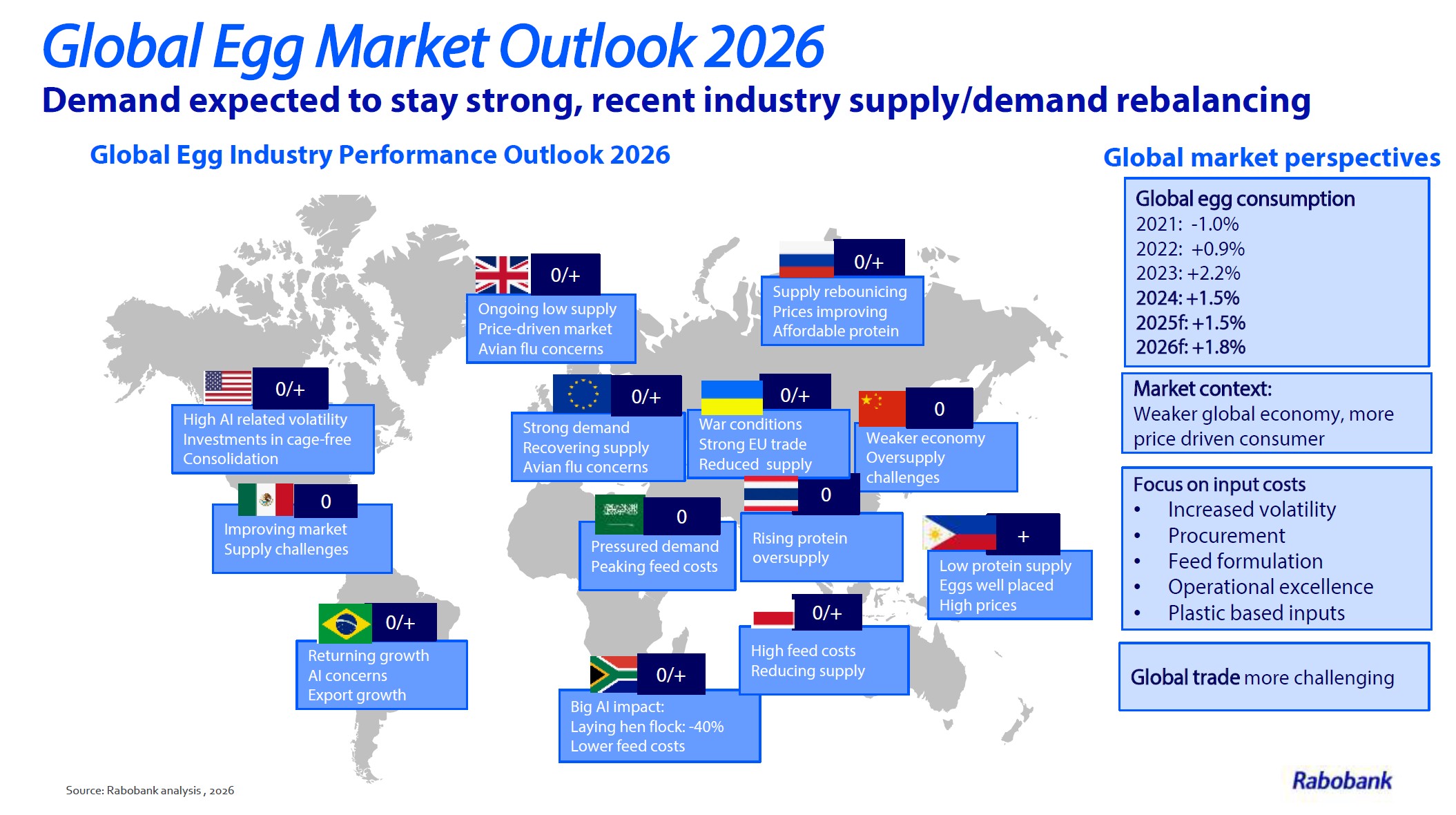

Global egg market outlook

Biofuels remain a structural demand driver. Global mandates are expanding, with both ethanol and biodiesel increasing their share of agricultural output. In Brazil, corn-based ethanol is becoming a major force, with its share of corn use expected to double over the coming years.This is reinforcing competition between feed, fuel and food markets, tightening the overall balance when supply is disrupted.Geopolitics continues to reshape global trade flows. US tariffs and wider trade tensions are influencing agricultural markets, but the most significant development remains the shift in China’s soybean sourcing. Imports from the US have declined sharply in recent years, with Brazil taking a larger share.

Iran conflict has significant potential impact on agrifood

Mulder noted that any change in trade relations could quickly alter that balance. China remains the dominant global buyer, and even small shifts in purchasing patterns have the potential to move markets significantly.Weather risk is also returning to the outlook. El Niño conditions are expected to strengthen through the year, increasing the likelihood of dry conditions in parts of the southern hemisphere and adding further uncertainty to production forecasts.Across the market, opposing forces are now clearly in play. High stocks, slower economic growth and weaker demand are acting as a stabilising influence, while energy prices, fertiliser costs, biofuel expansion and geopolitical disruption are pulling in the opposite direction.The result is a market that remains broadly balanced but increasingly sensitive to external shocks.Demand trends are also shifting. Growth in global animal protein production is slowing, particularly in China, the EU and Brazil, which is moderating feed demand. Eggs remain relatively well positioned within the protein mix, supported by affordability and steady consumption growth.Feed cost exposure remains a central issue for egg and poultry producers. While pricing has stabilised in the short term, the risk profile is weighted towards further increases if disruption continues.Mulder highlighted the importance of cost management, noting that feed typically accounts for 60–70% of production costs. Procurement strategy, ration formulation and operational efficiency are becoming increasingly important as volatility returns to the market.Looking beyond the immediate outlook, the presentation pointed to a broader structural shift. Supply chains are becoming more regional, food security is rising up the political agenda and competition for resources is intensifying.The re-emergence of the food versus fuel debate, combined with ongoing geopolitical tension, is expected to keep agricultural markets more volatile than in previous decades.High stock levels continue to provide short-term stability, but the direction of travel will depend on how long current disruptions persist, particularly in energy and fertiliser markets, and how trade relationships evolve through the year.