Egg sector enters more complex phase as supply tightens

Published on : 20 Apr 2026

Dr Magdalena Kowalewska, Director of the Food and Agri Sector Analyses Bureau at BNP Paribas Bank Polska

The global egg market is entering a more complex phase, with steady demand running up against tighter supply, geopolitical uncertainty and a changing cost base, delegates at the World Egg Conference heard today.Dr Magdalena Kowalewska, Director of the Food and Agri Sector Analyses Bureau at BNP Paribas Bank Polska, outlined a sector that remains structurally robust but increasingly exposed to volatility. Eggs, she said, continue to stand apart from other animal proteins, with production still largely local despite growing consolidation in processing and distribution.That distinction continues to shape how the market behaves. While international trade in eggs and egg products is expanding, primary production remains fragmented and regionally anchored, limiting global flows compared with poultry meat. Data presented in Warsaw showed egg trade at just a fraction of poultry meat flows in value terms, reinforcing how regionally contained the sector remains.

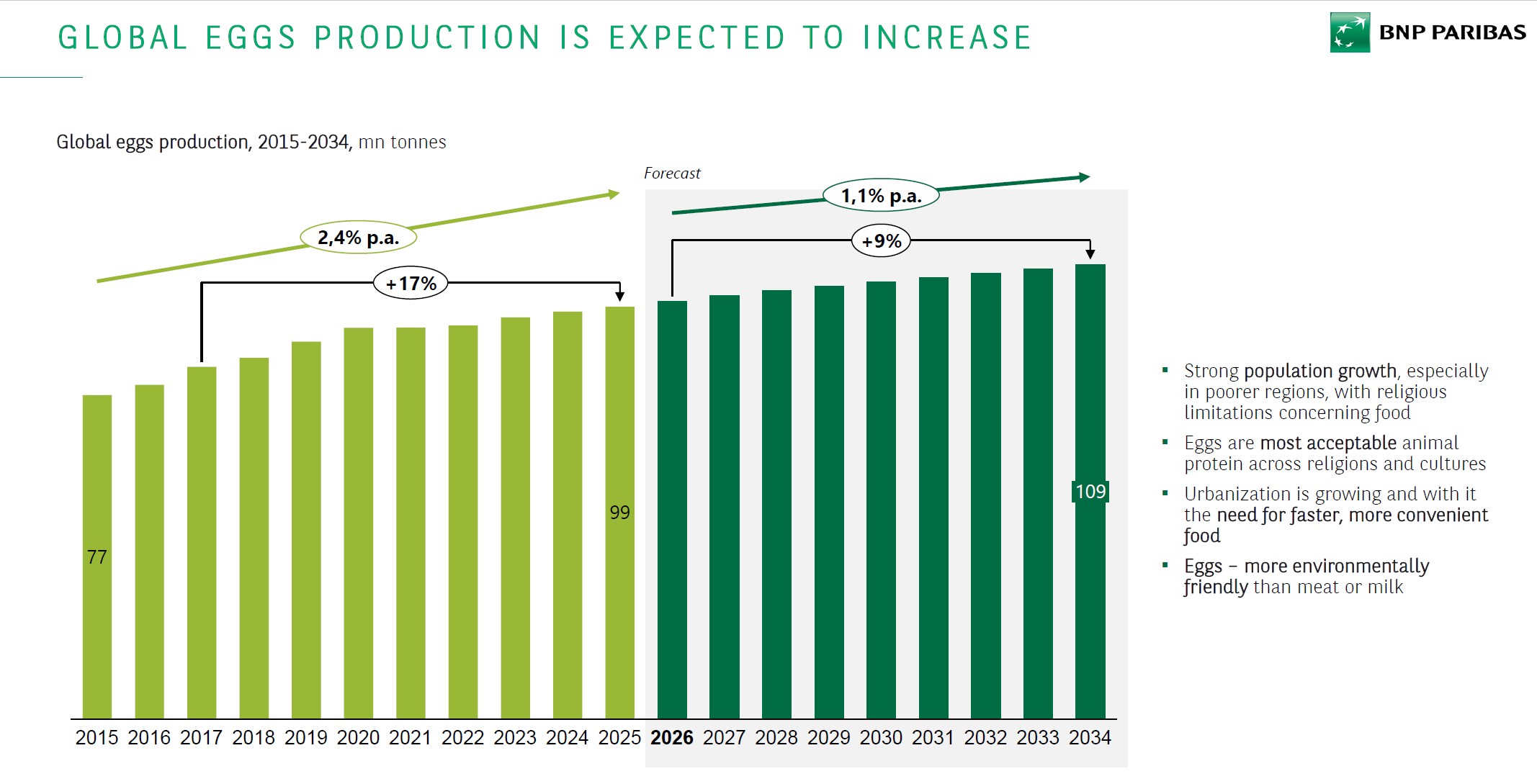

Global Egg Production is expected to increase

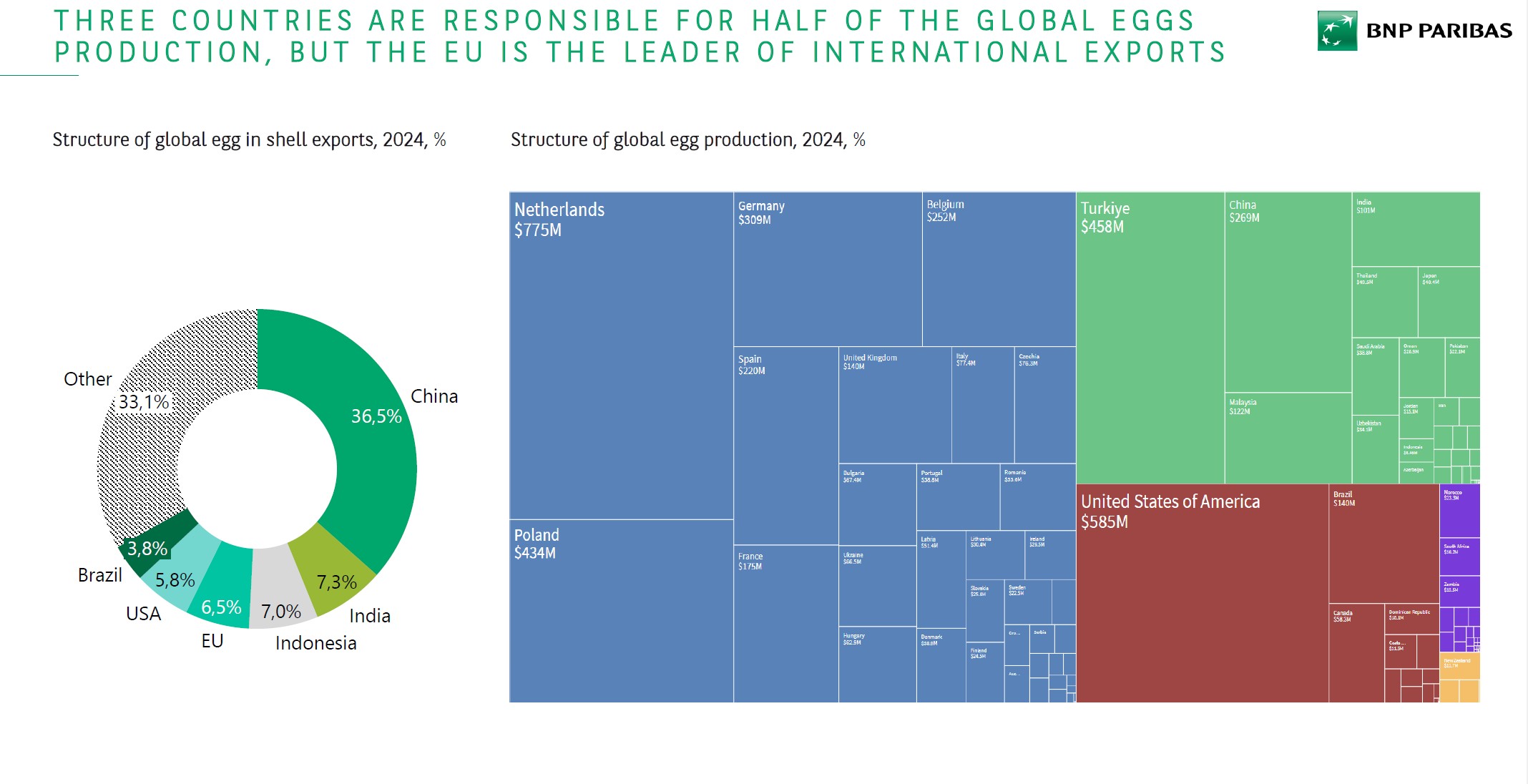

Global output is still forecast to rise, driven by population growth and increasing incomes, particularly in Asia and Africa. However, Kowalewska pointed to a clear slowdown in growth rates. Production is expected to move from roughly 99 million tonnes today to around 109 million tonnes by 2034, equivalent to growth of around 1.1 percent per year, compared with higher rates seen previously. Much of that increase is concentrated in Asia and Africa, where both production and consumption are rising in parallel, rather than export driven expansion.The structure of global supply remains highly concentrated. China alone accounts for more than a third of global production, with India, the EU, Indonesia and the United States forming the next tier. Despite that, the EU remains the leading exporter of eggs internationally, highlighting the gap between production concentration and trade leadership.

Three countries are responsible for half the global egg production

Conditions across key producing regions remain uneven. In parts of Asia, oversupply and weaker margins are weighing on producers, while in Indonesia supply is strong but prices remain volatile. In Europe, supply remains constrained, largely due to disease pressure. In the United States, production is recovering after avian influenza losses, with quarterly output beginning to move back towards long term averages and prices easing from peaks above $6 per dozen to closer to $3.The backdrop remains shaped by the after effects of the 2022 cost shock. Feed markets have stabilised since the surge in grain prices following the war in Ukraine, with FAO indices showing cereals and oils easing back significantly over the past two years. That has reduced immediate cost pressure, although prices remain above pre 2022 levels.Geopolitical risks remain firmly in play. The Middle East, as a key supplier of fertiliser, continues to influence the cost structure across the food chain. Disruption in the region feeds through into fertiliser pricing, fuel costs and broader supply chain volatility, with knock on effects across livestock production.

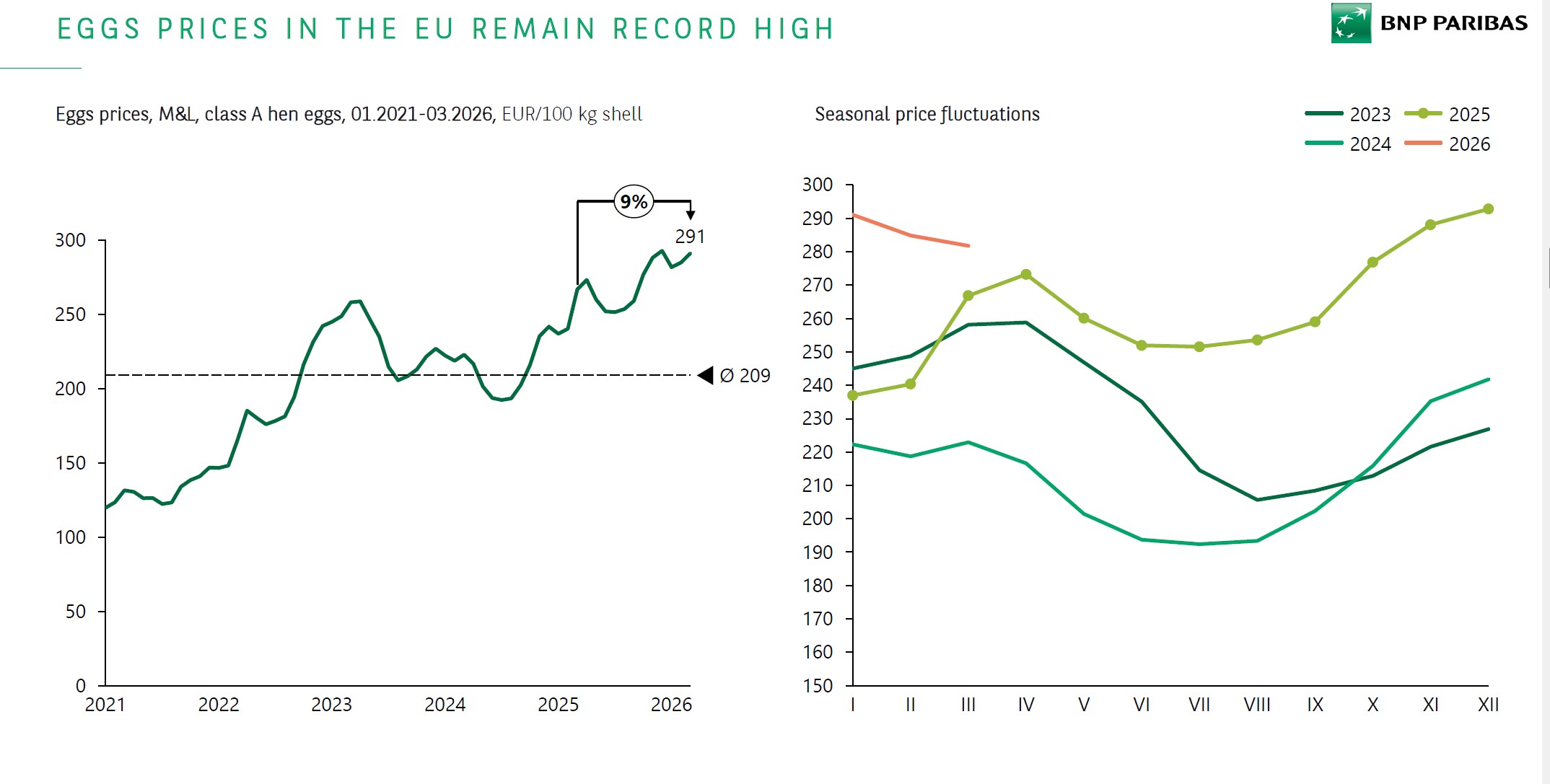

Egg prices in the EU remain at record high

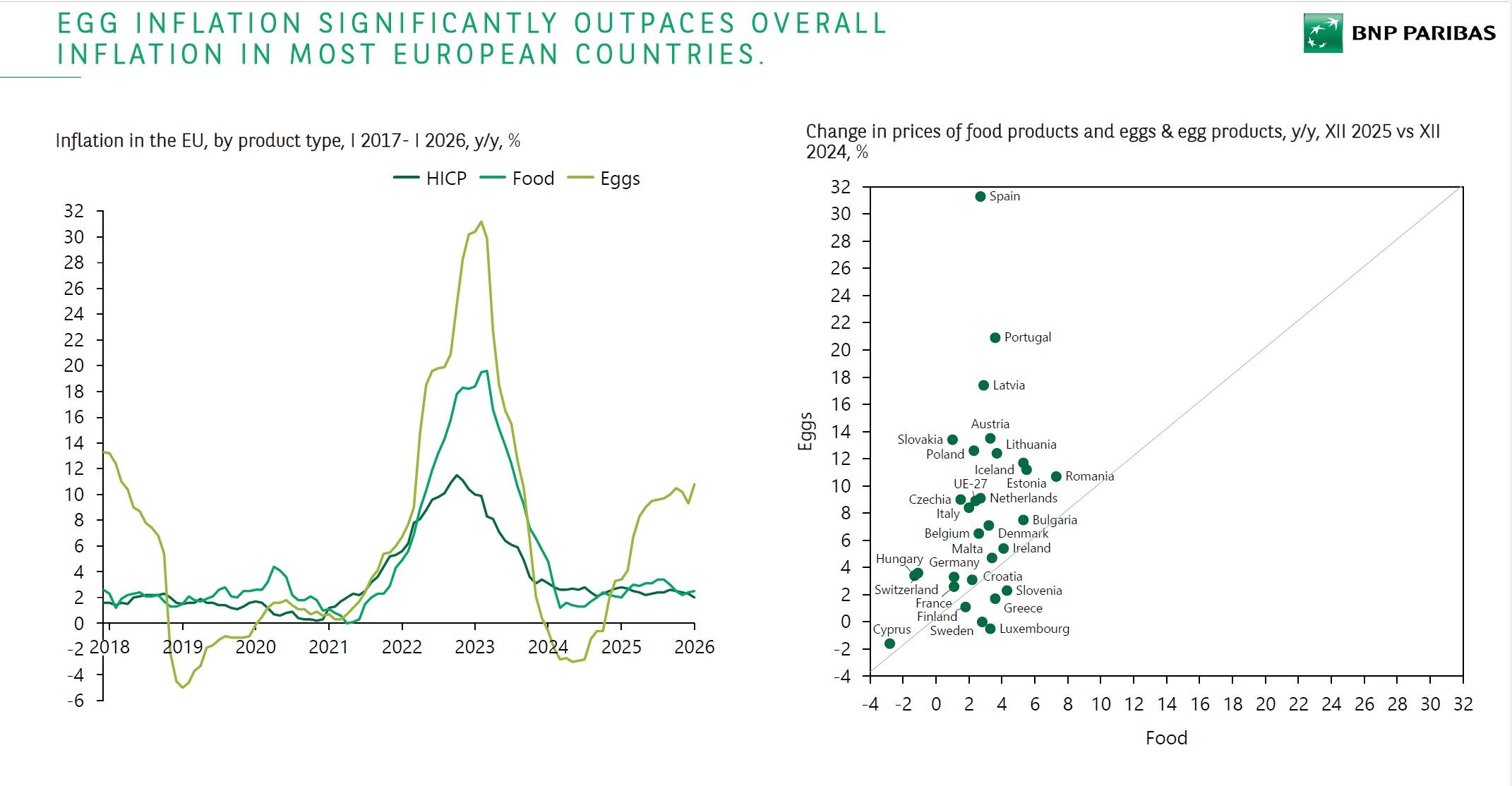

Disease continues to constrain supply in several regions. Avian influenza remains the dominant challenge, alongside Newcastle disease and salmonella. Mapping presented during the session showed ongoing outbreaks across Europe and North America, underlining the persistent nature of the risk rather than a one off event.Across the European Union, prices remain elevated by historical standards. EU egg prices have reached close to €300 per 100kg in recent cycles, with average levels still sitting well above long term norms. Inflation in eggs has also outpaced broader food inflation across most member states, with some countries seeing double digit increases where overall food inflation has been significantly lower.

Egg inflation significantly outpaces global inflation

Volatility differs by production system. Cage egg prices show the widest swings, while organic eggs have remained the most stable, with a coefficient of variation around 6 percent compared with double digit levels in other systems. Despite the ongoing shift in production models, cage and barn systems still account for more than three quarters of EU output, reflecting the scale of infrastructure still tied to those systems.Production volumes within the EU are broadly stable. Data on hatching eggs and laying hen numbers across major countries shows fluctuations year to year, but no sustained expansion. In countries such as Germany and the Netherlands, output has contracted in recent years, while others such as Poland have seen more variable patterns, including periods of stronger growth followed by correction.Trade flows are also shifting. While the EU maintains a positive trade balance overall, exports to the Middle East have fallen sharply. Shipments to the region have dropped by more than half compared with earlier levels, with the share of exports to those markets declining significantly over the past five years.Within the EU, the structure of the sector varies widely. Poland combines a concentrated packing sector with a fragmented production base and a strong export orientation. In contrast, countries such as France and Germany play a leading role in organic production, while Italy, Germany and France dominate overall output.On the demand side, the picture remains supportive. Consumption continues to rise globally, albeit slowly in mature markets. In the EU, per capita consumption sits around 14kg and is projected to increase only modestly over the next decade, reflecting the maturity of the market.

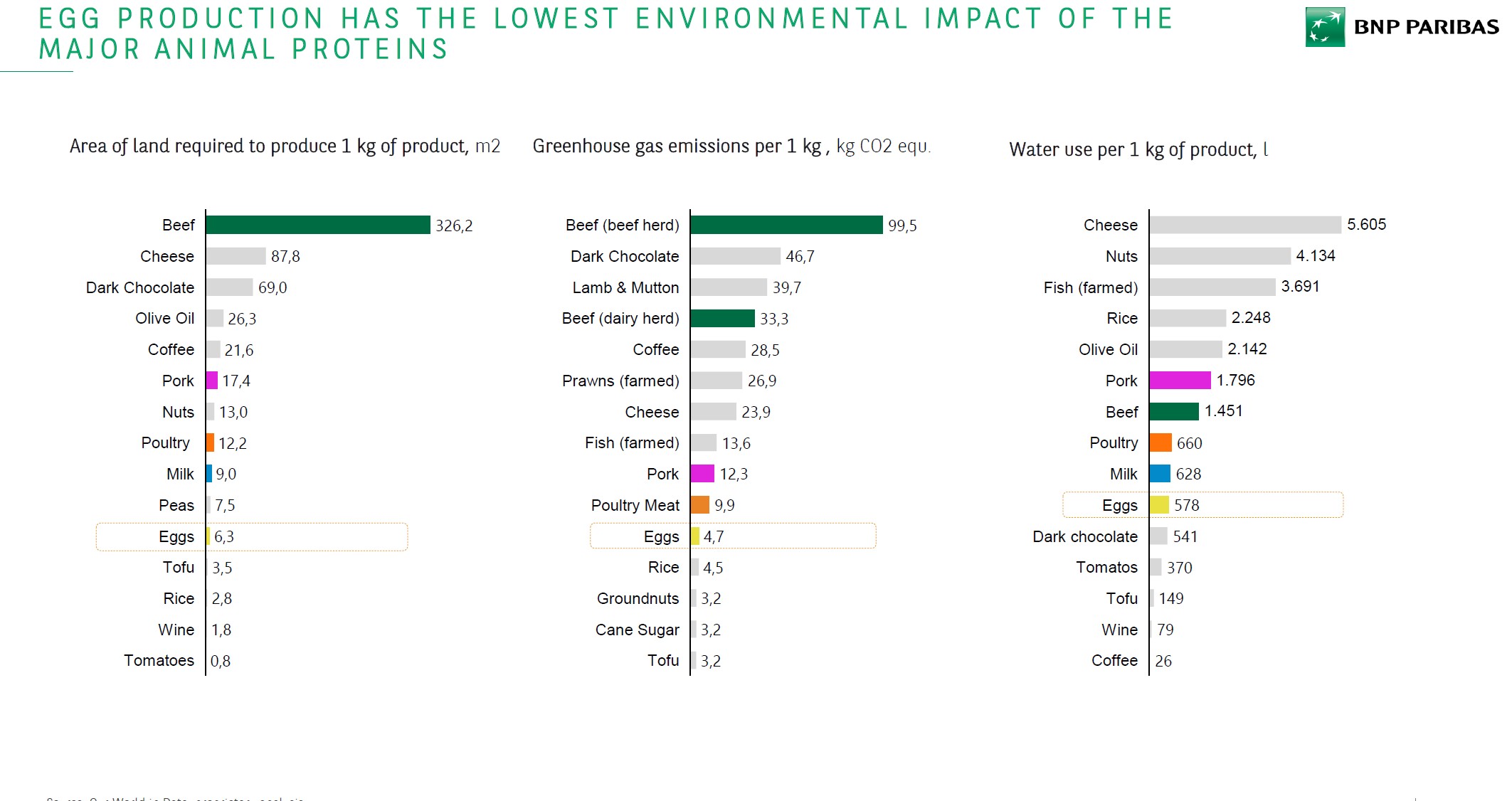

Egg production has lowest environmental impact of all the major animal proteins

Globally, consumption patterns vary widely. Higher intake is concentrated across Europe, North America and parts of Asia, while lower consumption levels remain in parts of Africa and the Middle East, pointing to longer term growth potential tied to income and urbanisation.Even in markets where prices have increased significantly, demand has held up well. In the United States, 87 percent of consumers reported eating eggs within a recent six month period, with only a small minority expecting to cut back despite higher prices. Eggs continue to score strongly on convenience, affordability and everyday use.They also remain embedded in daily eating habits. Consumer data presented showed eggs consistently ranking among the most commonly consumed breakfast items across major European markets, alongside bread, cereals and dairy products.Consumer preferences are shifting in ways that continue to favour the category. Across multiple regions, shoppers are prioritising natural ingredients, high protein content and nutritional value. In markets such as China and India, health related attributes rank particularly highly, while in Europe naturalness and vitamin content remain key drivers.Product positioning reflects those differences. In Europe, product launches are dominated by ethical and sustainability claims, particularly animal welfare, environmentally friendly packaging and organic production. In other regions, branding, convenience and digital influence carry more weight, with social media playing a growing role in product visibility.On the environmental side, eggs continue to compare favourably with other animal proteins. Data presented showed significantly lower greenhouse gas emissions per kilogram than beef, pork or dairy, alongside lower land use and water requirements, reinforcing their position within lower impact protein categories.Retail pressure continues to shape production systems. Major chains across Europe and North America are progressing towards cage free supply targets, with some already reaching full conversion in key markets and others setting timelines extending towards the end of the decade.